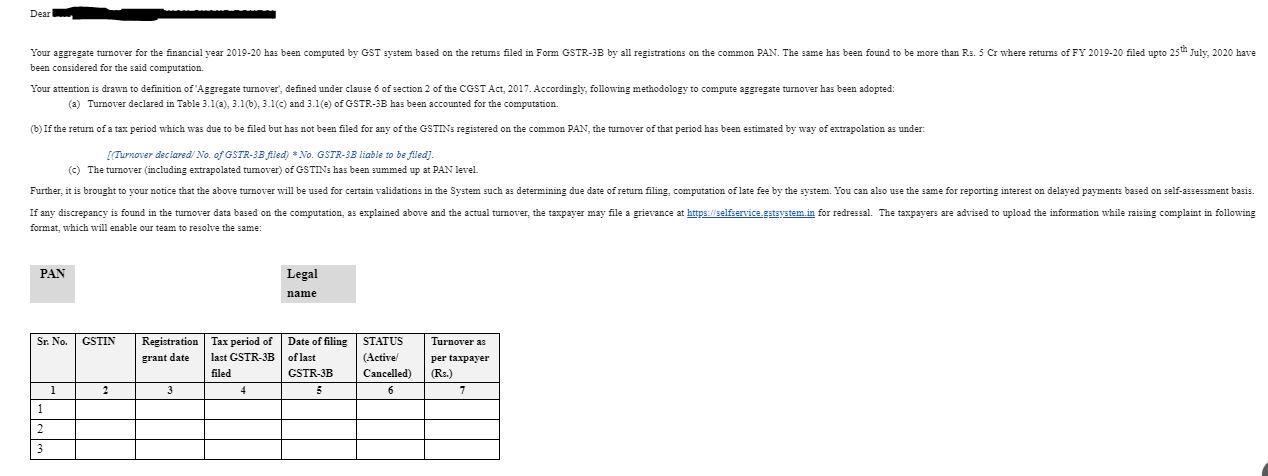

Email from GSTN (noreply@gstn.gov.in) – Registered persons whoes Aggregate turnover being more than Rs. 5 Cr during FY 2019-20 has received an email from GST Department (GSTN)

You may have received an email from GSTN on 04/05th August, 2020 about Aggregate turnover being more than Rs. 5 Cr during FY 2019-20. Here we will discuss few take aways and Action points the registered person under GST needs to take in mind (Sample e-mail received from the GST department has been attached at the end of this article).

The summary and probable explanation of the email is as under –

Aggregate turnover for the financial year 2019-20 has been computed by GST system based on the returns filed in Form GSTR-3B by all registrations on the common PAN which exceeds Rs. 5 Cr. The returns of FY 2019-20 filed upto 25th July, 2020 have been considered for the said computation.

Computation of Aggregate Turnover –

‘Aggregate turnover’, has been computed as per defined u/s 2(6) of the CGST Act, 2017. Same has been computed based Sum of the turnover as declared in GSTR 3B in below tables –

Table 3.1(a) – Outward taxable supplies (other than zero rated, nil rated and exempted)

Table 3.1(b) – Outward taxable supplies (zero rated)

Table 3.1(c) – Other Outward Taxable supplies (Nil rated, exempted); and

Table 3.1(e) – Non-GST Outward Supplies

Methodology of Computation of Aggregate Turnover – Same is computed as per one of the methods-

Option 1 – Sum of the turnover as declared in GSTR 3B filed for all tax periods for 2019-20

Option 2 – Return of a tax period which was due to be filed but has not been filed for any of the GSTINs registered on the common PAN, the turnover of that period has been estimated by way of extrapolation as under

[(Turnover declared/ No. of GSTR-3B filed) * No. GSTR-3B liable to be filed]

Option 3 – The turnover (including extrapolated turnover) of GSTINs has been summed up at PAN level

Relevance/ Application of such Computation:

It is relevant for the registered persons who’s turnover is less then Rs. 5 crore and still they have received the email from the department.

The above turnover will be used for certain validations in the System such as

- Determining due date of return filing (20th or 22nd or 24th of subsequent month for GSTR 3B)

- Computation of late fee by the system

- Reporting interest on delayed payments based on self-assessment basis (based on recent relief announced due to outbreak of Covid -19)

Action Point for registered person: In case of any discrepancy in email provided to you:

If any discrepancy is found in the turnover data based on the computation, as explained above and the actual turnover:

a. the taxpayer may file a grievance at https://selfservice.gstsystem.in for redressal.

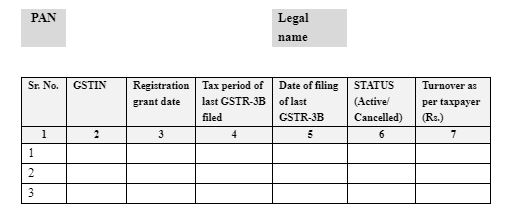

b. The taxpayers are advised to upload the below information while raising complaint in following format, which will enable the GSTN team to resolve the same.

Format in which information needs to be shared while raising compliant:

Sample e-mail received from the GST department has been attached at the end of this article: