What is ITC?

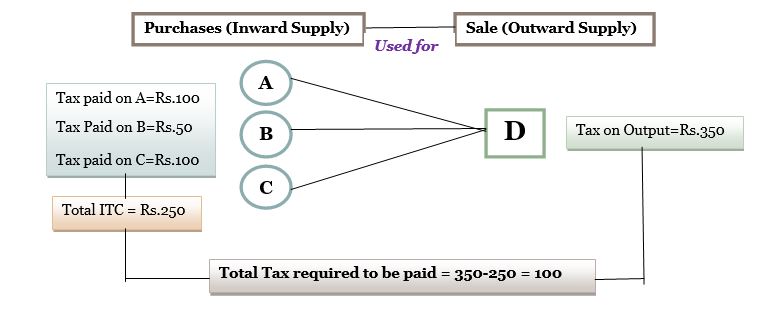

ITC – Input Tax Credit is the tax paid on inward supply of goods/services (e.g. purchases) that can be reduced when paying the Output liability.

Example:

Conditions for claiming ITC:

- Payment shall be made within 180 days.**

- Used for business purposes.

- Actual possession of invoices/debit notes/credit notes/bill of supply etc.

- Receipt of goods/services.

- Tax has been actually paid by the supplier.

- No ITC will be allowed if depreciation has been claimed on the tax component of capital goods

*If Inputs are received in lots – Can claim ITC only when the last lot is received.

**If not, ITC claimed will be added to the output liability along with interest. However, once the amount is paid, ITC can be re-claimed.

Time limit for claiming ITC?

- Due date of furnishing of next year’s september’s return (to which such invoice pertains)

Or

- Furnishing of relevant annual return

Whichever is earlier.

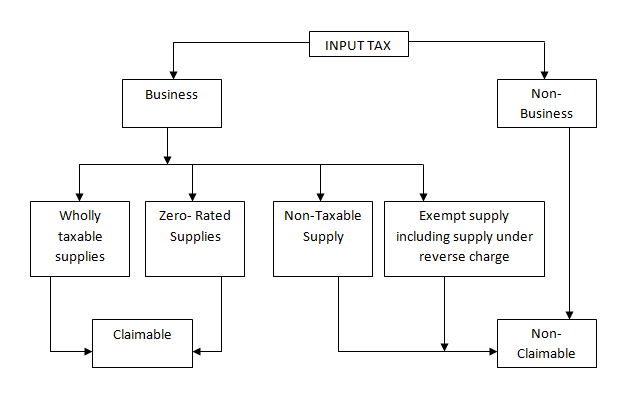

When to avail and not to avail ITC under GST: